New

Energy

Outlook

2022

The New Energy Outlook (NEO) is BloombergNEF’s long-term scenario analysis on the future of the energy economy covering electricity, industry, buildings and transport and the key drivers shaping these sectors until 2050.

This edition presents detailed country-level energy and climate scenarios for corporates, financial institutions and policy makers navigating the energy transition.

The Economic Transition Scenario is our baseline assessment of how the energy transition might evolve from today as a result of cost-based technology changes.

The Net Zero Scenario describes an economics-led evolution of the energy economy to achieve net-zero emissions in 2050. This scenario combines faster and greater deployment of renewables, nuclear and other low carbon dispatchable technologies in power with the uptake of cleaner fuels in end-use sectors, most notably hydrogen and bioenergy. Taking a sector-led approach, it describes a credible pathway to meet the goals of the Paris Agreement.

To give you an even deeper dive into some of the sectors and regions covered in the New Energy Outlook, our analysts have developed additional reports available here.

NEO 2022 Key Messages

1. Emissions

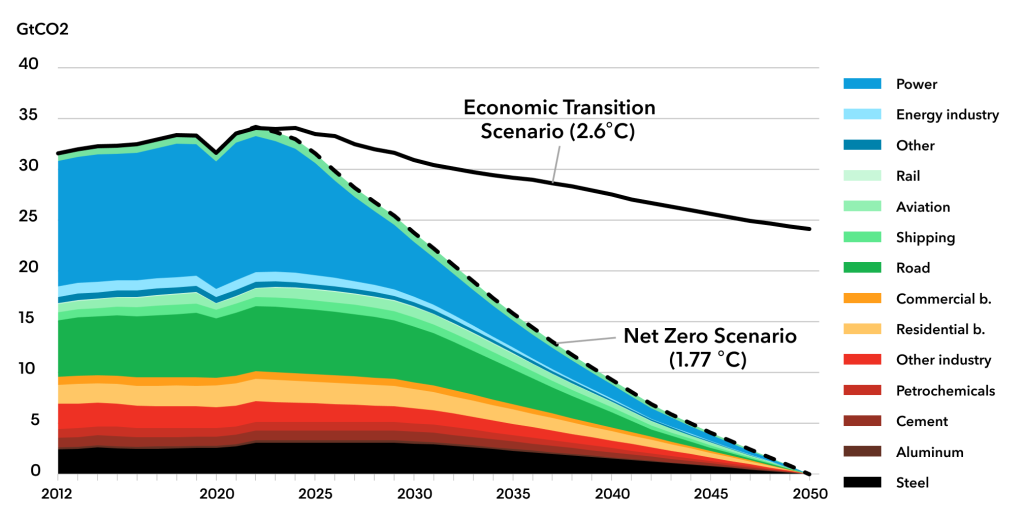

The energy transition in the power sector is well under way and global power sector emissions have most likely peaked in 2022. In order to stay on track for net zero, emissions in all sectors need to peak now and start declining fast.

In the Net Zero Scenario, transport sector emissions peak in 2024 and fall quickly due in particular to the electrification of road transport. Industrial sector emissions are already leveling off and then begin their steep decline in 2030. Building-sector emissions, already far lower than industrial or transport emissions, decline relatively slowly from a peak this year. By comparison, industry and buildings emissions both increase through 2050 in the Economic Transition Scenario (ETS), albeit slowly.

Economic Transition Scenario

Source: BloombergNEF

2022

2028

2044

2050

2017

MtCO2

Net Zero Scenario

Source: BloombergNEF

2022

2024

2014

2022

2017

MtCO2

Economic Transition Scenario

Source: BloombergNEF

2022

2028

2044

2050

2017

MtCO2

Net Zero Scenario

Source: BloombergNEF

2022

2024

2014

2022

2017

MtCO2

Economic Transition Scenario

Source: BloombergNEF

2022

2028

2044

2050

2017

MtCO2

Net Zero Scenario

Source: BloombergNEF

2022

2024

2014

2022

2017

MtCO2

2. Carbon Budgets

Our modelling shows that, while a pathway that limits global temperature increases to 1.5 degrees Celsius by 2050 looks increasingly out of reach, there are still plausible pathways to stay within 1.77C of warming in our Net Zero Scenario. Even then, a revolution will be needed in the energy sector to increase momentum and accelerate emissions reductions.

Our modelling suggests emissions need to fall by 30% by 2030 and overall 6% a year to 2040. If achieved, this orderly transition would reach zero emissions in 2050 and achieve the Paris Agreement objective, with climate change of 1.77C by 2050, without overshooting or creating the need for net-negative emissions post-2050. In contrast, emissions in our Economic Transition Scenario fall at 0.9% on average each year, resulting in emissions consistent with 2.6C warming trajectory by the end of the century.

Source: BloombergNEF

3. Abatement

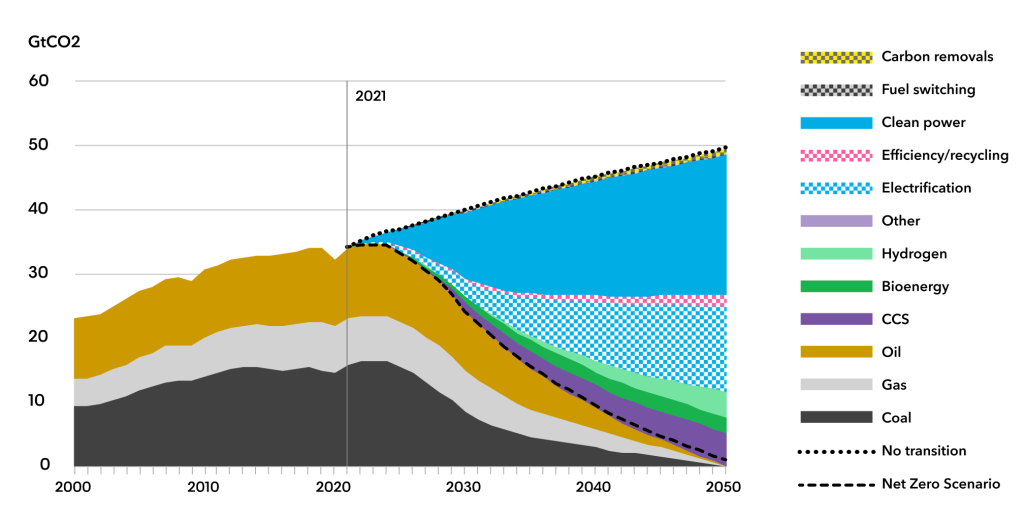

Switching power generation from fossil fuels to clean power is the single biggest contributor to global emission reductions in our Net Zero Scenario, accounting for half of all emissions abated over 2022-50. This includes displacing unabated fossil fuel with wind, solar, other renewables and nuclear. Electrification of transport and industrial processes, buildings and heat – using increasingly lower-carbon electricity – is the next biggest contributor, abating about a quarter of total emissions over the period. Hydrogen is a sizeable contributor as well in absolute terms, though significantly smaller in relative terms, accounting for about 6% of reductions.

CCS gains in importance from the early 2030s, as hard-to-abate sectors are being tackled and unabated fossil fuel plants are retrofitted with the technology. CCS accounts for 11% of all emissions abated over the scenario period.

CO2 emissions reductions from fuel combustion, Net Zero Scenario versus no transition scenario

Source: BloombergNEF. Note: The ‘no transition’ scenario is a hypothetical counterfactual. In the power and transport sector, it keeps the current fuel mix constant at 2021 levels, with emissions growing proportionally to forecast energy demand. For all other sectors, the counterfactual to the Net Zero Scenario (NZS) is the Economic Transition Scenario (ETS). ‘Clean power’ includes renewables and nuclear. ‘Bioenergy’ refers to direct use outside the power sector. ‘Efficiency/recycling’ includes demand-side efficiency gains in aviation, shipping and buildings, and greater recycling in industry.

4. Primary Energy

In our Net Zero Scenario, oil, gas and coal consumption all peak nearly immediately, if they have not done so already. Under this scenario global coal demand peaks in 2022, gas demand peaked in 2021, and oil demand peaked in 2019, before the Covid-19 pandemic. For oil and gas, this is a marked departure from the trajectories in our Economic Transition Scenario.

5. End Use Sectors

Final energy use in the Net Zero Scenario has very different profiles for each sector. This is due to several factors, but first among them is electrification of transport, industrial processes and heat.

Source: BloombergNEF

6. Electrification

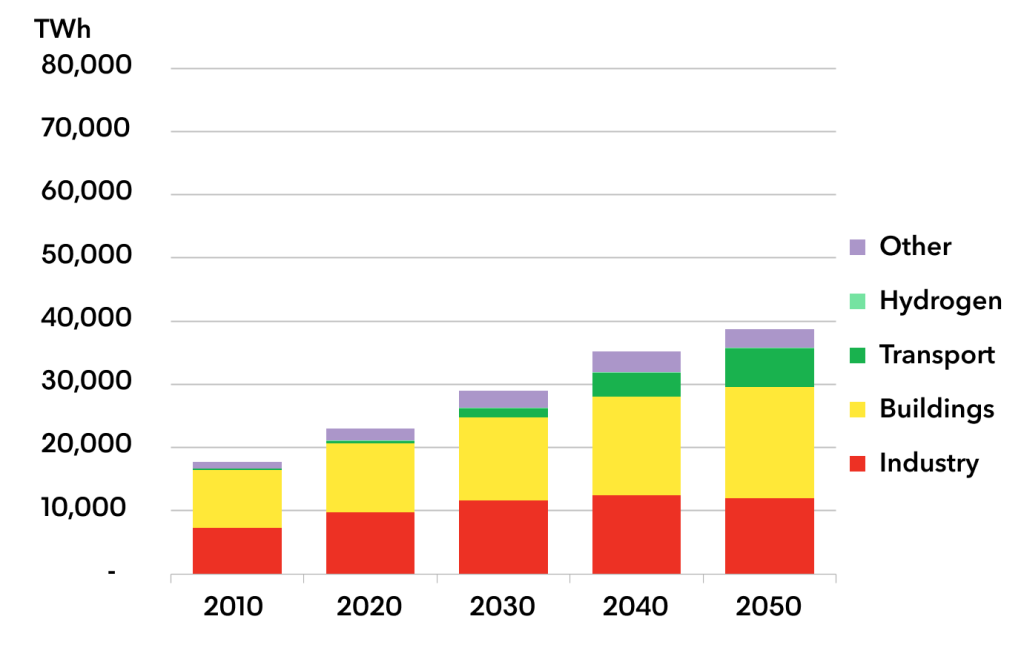

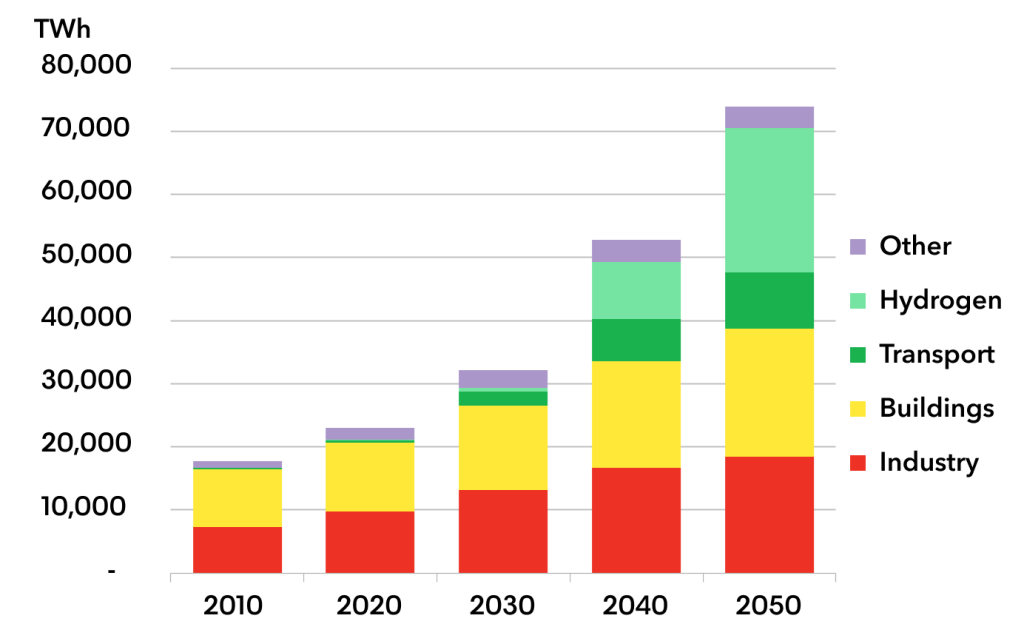

Reaching net-zero emissions by mid-century requires a significant increase in global electricity generation. The Energy Transition Scenario requires 46,000 terawatt-hours of power generation in 2050, nearly double today’s amount. The Net Zero Scenario, however, requires more than 80,000 terawatt-hours of generation, more than triple today’s amount.

Power demand from hydrogen, which is insignificant in the Economic Transition Scenario, is close to 23,000TWh per year in the Net Zero Scenario by mid-century as we assume that 88% of hydrogen production is achieved via grid-connected electrolyzers. That makes hydrogen the single biggest source of power demand globally by 2050, equal to total global demand in 2020.

Sources of global power demand

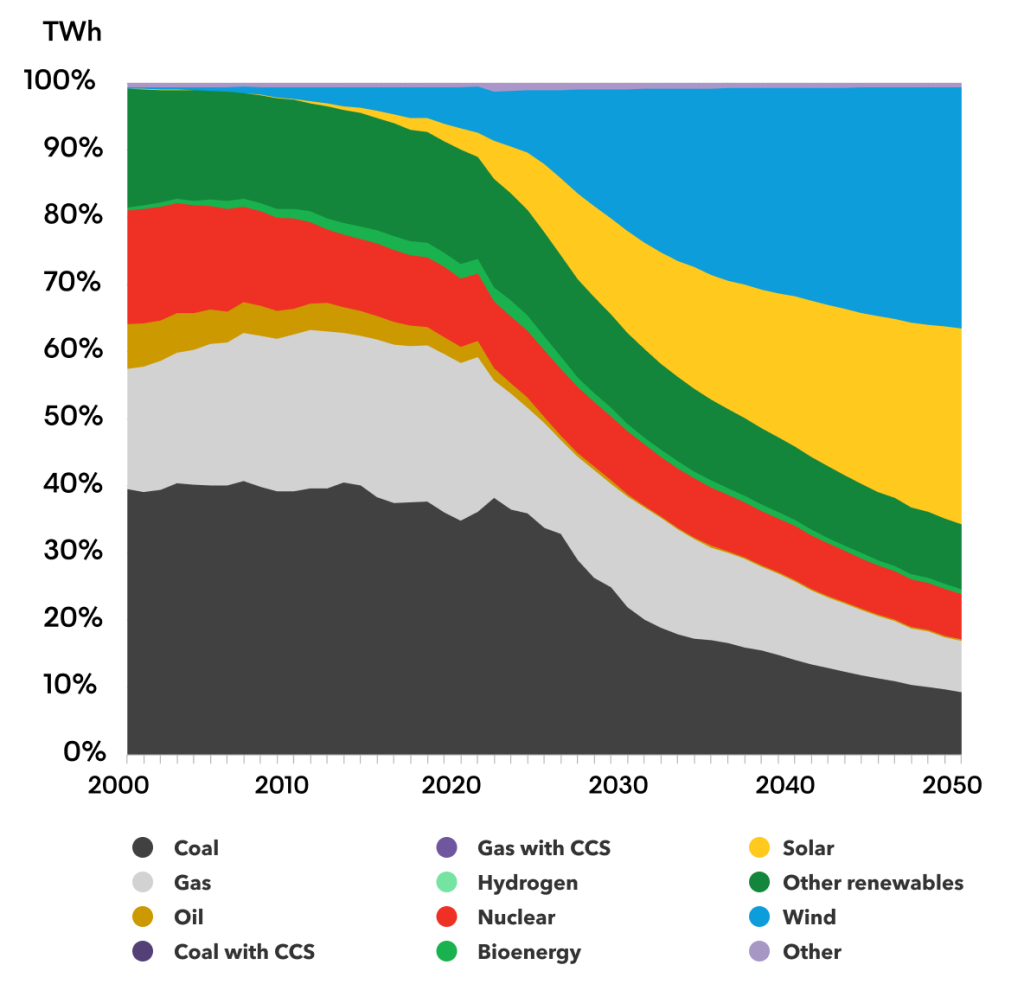

Economic Transition Scenario

Source: BloombergNEF

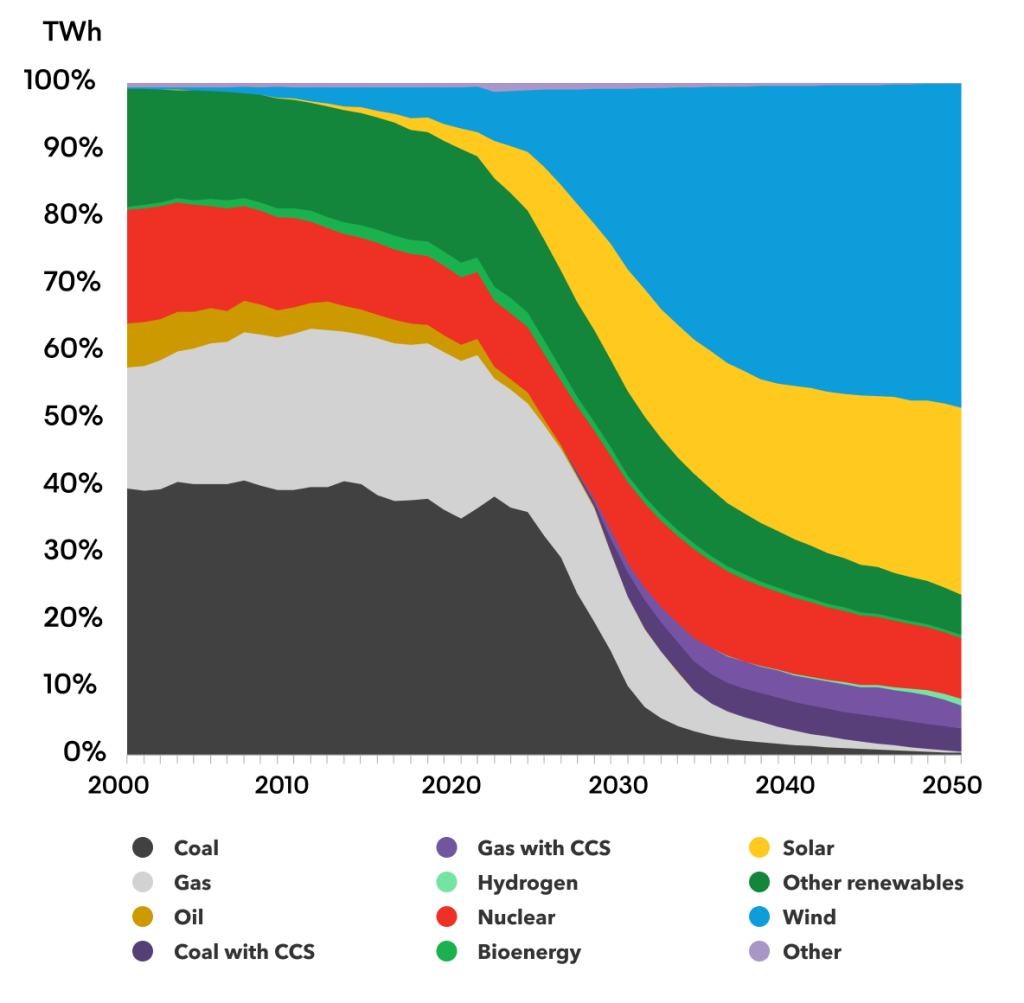

Net Zero Scenario

Source: BloombergNEF

7. A Low-Carbon Power System

In addition to increasing total power generation significantly, the Net Zero Scenario requires a significant change in the production mix. This is not an evolution of the Economic Transition Scenario – it is effectively a completely different power system.

Reaching net zero will result in almost zero fossil fuel-fired power generation operating without carbon capture and storage; it will also require more nuclear power generation, and even more wind and solar power to be deployed. In the Net Zero Scenario, wind and solar power are more than three-quarters of total power generation.

Electricity generation by technology, by scenario

8. CCS and Hydrogen

Carbon capture and storage and hydrogen emerge as major technologies for deep decarbonization, with applications across industry, power, buildings and transport. We estimate that about 7 gigatons of carbon dioxide will need to be captured annually in 2050 – the equivalent of today’s power sector emissions from Europe, China and India combined. Hydrogen production will rise to 500 million metric tons annually in 2050, a fivefold increase from today’s levels.

500MtH2

Million metric tons of hydrogen demand, 2050

7GtCO2

Gigatons of carbon dioxide captured, 2050

Source: BloombergNEF

9. The Need for Deep Decarbonization

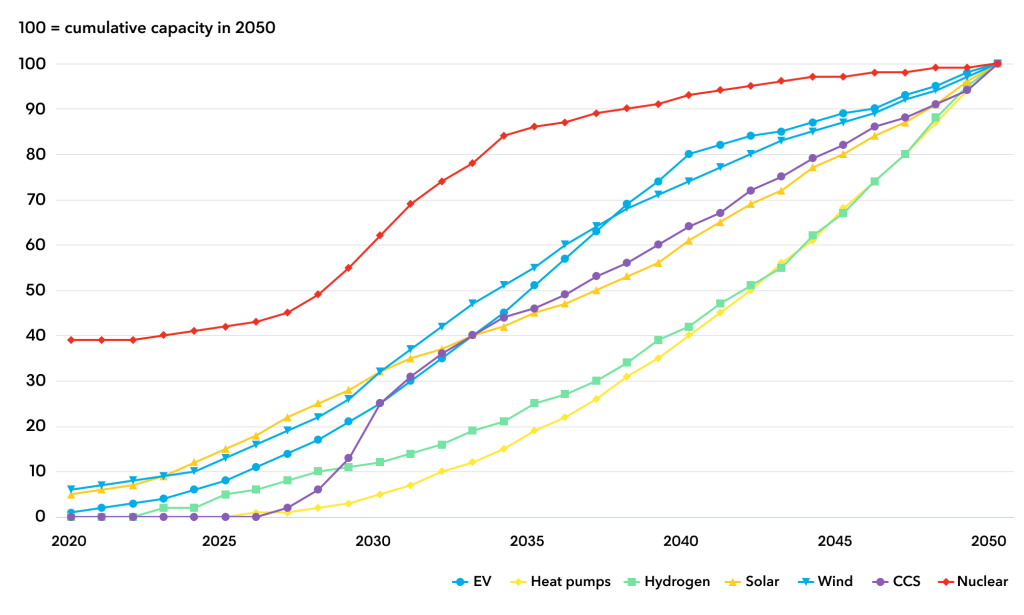

The net zero transition is still in its infancy. Each of these key technologies is still at a fraction of the scale that is needed. Today, more than 40% of the nuclear power capacity needed in 2050 already exists, but less than 10% of the necessary total wind and solar has been installed, and effectively none of the heat pumps, hydrogen electrolyzers, or CCS capacity that are needed.

That said, the ramp rates needed for the four technologies that do exist today – electric vehicles, wind, solar and nuclear power – are very different. Each of these technologies reach peak annual deployments considerably higher than today’s levels. Electric vehicle sales will need to increase fivefold, from under 11 million to 55 million per year, in order to satisfy net-zero targets and meet sector carbon budgets. Solar installations will need to more than triple and wind installations will need to increase sixfold.

Source: BloombergNEF Note: Wind, solar, carbon capture and storage (CCS), and nuclear uptake based on installed capacity in the power sector. Electric vehicle (EV) uptake based on passenger electric vehicle annual sales as modeled under BNEF’s New Energy Outlook Net Zero Scenario. Heat pumps based on fuel consumption for residential heat pumps. Hydrogen uptake based on power demand from grid-connected electrolyzers.

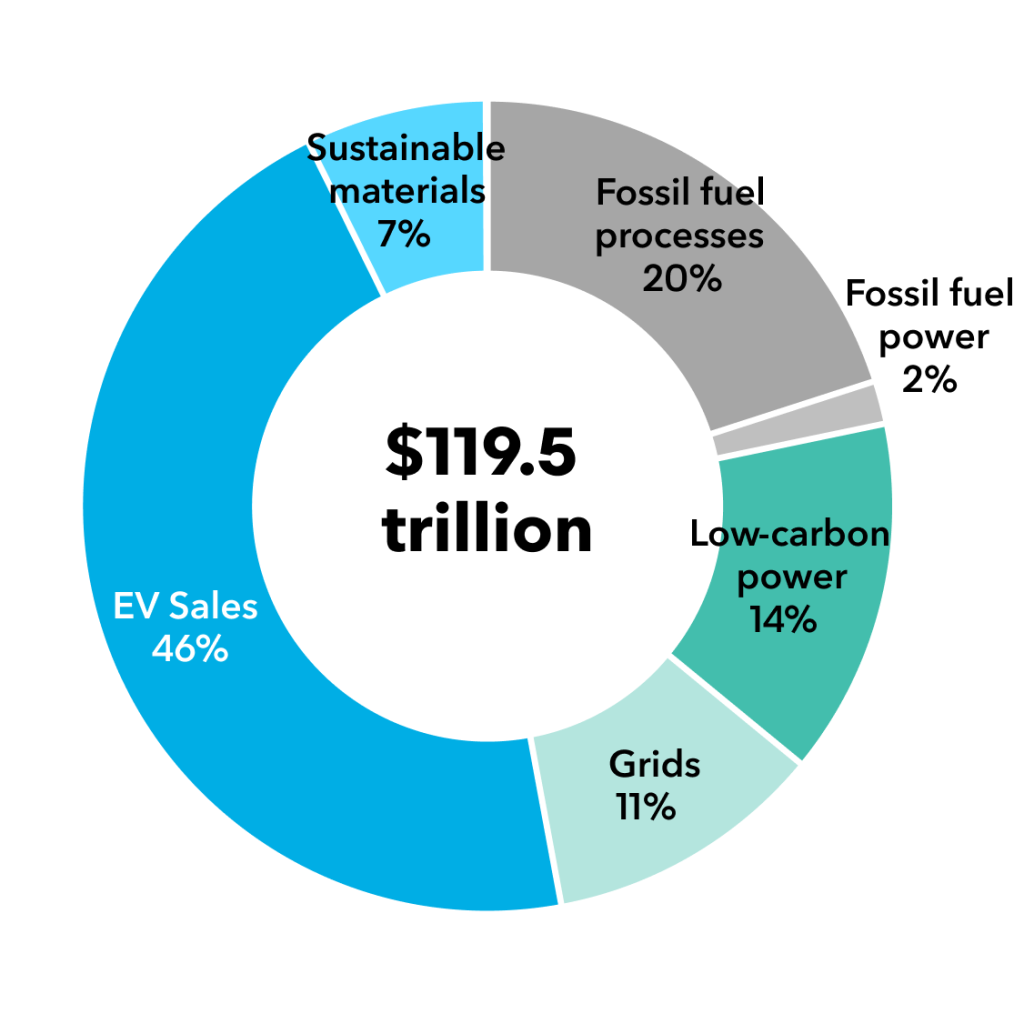

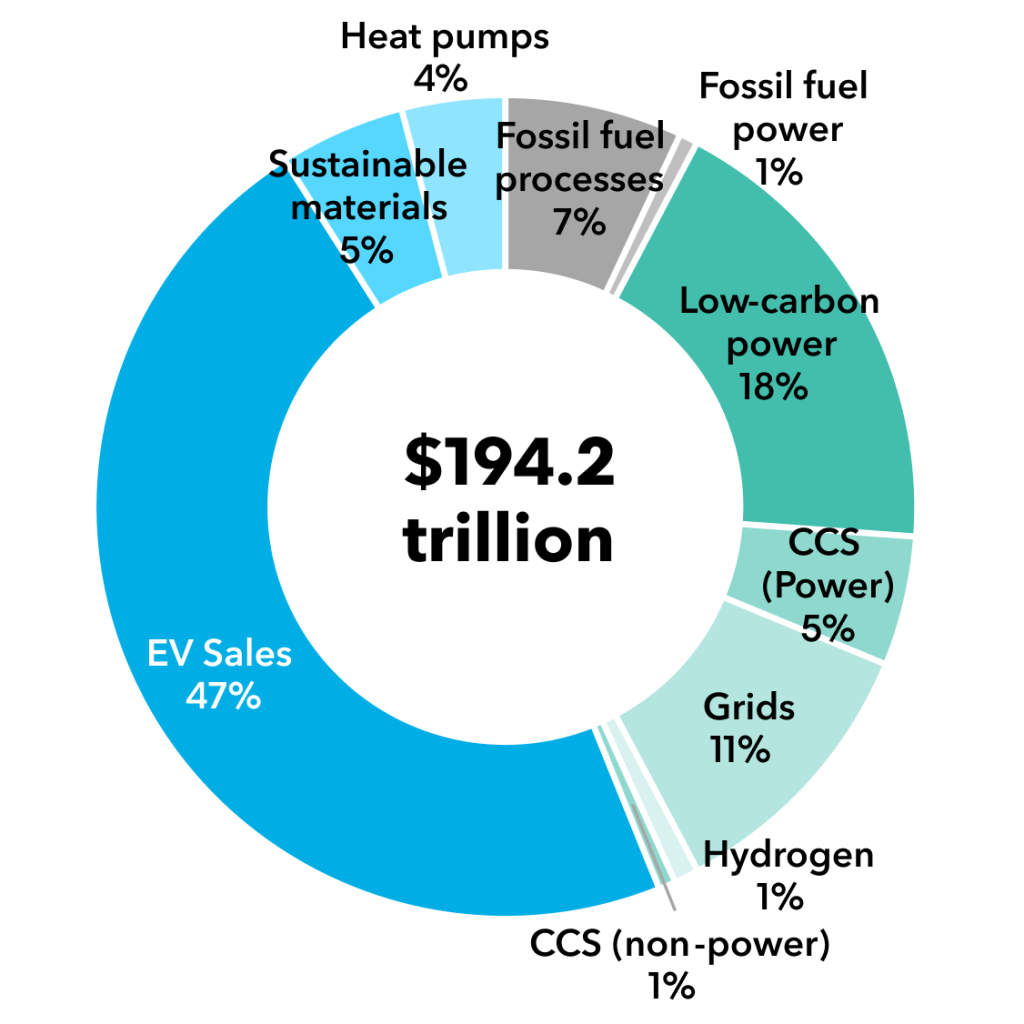

10. Investments

Getting to net zero is a multi-trillion investment opportunity, but to stay on track will require a shift away from fossil-fuel investment. To stay on track in the Net Zero Scenario, this means that for every dollar invested in fossil energy supply, nearly five are invested into low-carbon supply through 2050.

Note: Carbon capture and storage (CCS) includes investment in power sector (fossil fuel plant and CCS equipment), industry and blue hydrogen production (CCS equipment), as well as storage and transport infrastructure across all sectors.

Executive summary

High-level findings of NEO 2022 are available in the free executive summary below.

Report authors

David Hostert

Head of Economics & Modeling, Lead author

Matthias Kimmel

Head of Energy Economics

Dr. Ian Berryman

Lead Modeler

Amar Vasdev

Energy Economics

Nathaniel Bullard

Content

Hugh Bromley

Content

Dr. Kwasi Ampofo

Metals

Albert Cheung

Head of Research

Sanjeet Sanghera

Grids

Claudio Lubis

Investment

Meredith Annex

Hydrogen

With support from

Vicky Adijanto

Indonesia

Felicia Aminoff

Europe

Ali Asghar

Coal

Dr. Julia Attwood

Industry

Emma Champion

Europe

Jenny Chase

Solar

Caroline Chua

Indonesia

Robert Clarke

Product

Jennifer Cogburn

Gas

David Doherty

Oil

Isabelle Edwards

Product

James Ellis

Latin America

Ryan Fisher

Electric vehicle charging

Chris Gadomski

Nuclear

Andreas Gandolfo

Europe

Logan Goldie-Scot

Clean power

Andrew Grant

Electric vehicles

Yuchen Huo

Metals

Dr. Ali Izadi-Najafabadi

Asia-Pacific

Atin Jain

Asia-Pacific

Shantanu Jaiswal

India

David Kang

Japan

Takehiro Kawahara

Aviation

Nannan Kou

China

Minky Lee

Design

David Lluis Madrid

CCS

Sofia Maia

Energy transitions

Fauziah Marzuki

Gas

Nell Matthews

Marketing

Colin McKerracher

Transport

Oliver Metcalfe

Wind

Tara Narayanan

US

Kostas Pegios

Modeling

Leonard Quong

Australia

Abhishek Rohatgi

Gas

Dr. Tom Rowlands-Rees

Americas

Yayoi Sekines

Batteries

Ashish Sethia

Commodities

Seohee Song

Energy Economics

Dr. Nikolas Soulopoulos

Commercial transport

Sisi Tang

Petrochemicals

Martin Tengler

Hydrogen

Allen Tom Abraham

Indonesia

Andrew Turner

Modelling

Mohith Velamala

Shipping

Ben Vickers

Editorial

Hanyang Wei

China

William Young

Investment

Ethan Zindler

Americas